“Get the credit card that plants a tree with every purchase,” prompts the text of a Facebook ad for Aspiration’s Zero credit card (tagline: One Card. Zero Footprint). The ad was visible to people of any gender based anywhere in the U.S., but the advertiser asked that Facebook not show it to anyone under 25.

Another ad, for Hometap, a service providing cash in exchange for shares in home equity, was also broadcast to Facebook users across the U.S. but could not be seen by anyone whose age was listed as below 35.

The Markup found examples of four different companies targeting ads for financial services to restricted age groups, a practice that violates Facebook’s anti-discrimination policies and, in some cases, may violate federal or state civil rights laws. Two companies that ran such ads—Chime and Aspiration—had already been identified in a November 2019 lawsuit brought by civil rights groups against Facebook for age-restricting financial ads. (Chime and Aspiration were not defendants in the case.) The case was dismissed without prejudice.

In March 2019, after a separate set of legal actions, Facebook agreed to a settlement with civil rights groups in which it agreed to prohibit advertisers from targeting ads for housing, employment, and credit opportunities by age, race, national origin, or gender. The company did not admit to any wrongdoing and has consistently argued in court that it is not liable for the choices advertisers make on its platform.

Galen Sherwin, a senior staff attorney with the ACLU’s Women’s Rights Project, who was one of the attorneys involved in the 2019 settlement, said the ads The Markup found likely do not violate that agreement.

We have policies around when people can use certain targeting criteria. We don’t allow that for certain types of advertisements, such as financial services advertisements, or housing advertisements.

Monika Bickert, Facebook

“The settlement agreement doesn’t require perfect systems, because no such things exist,” Sherwin said. “But when there are issues detected with the efficacy of the classifiers, we can present that to Facebook and they are supposed to take that into account.”

Facebook’s vice president for content policy, Monika Bickert, reiterated the anti-discrimination policy during a Senate Judiciary subcommittee hearing earlier this week.

“We have policies around when people can use certain targeting criteria,” Bickert said. “We don’t allow that for certain types of advertisements, such as financial services advertisements, or housing advertisements.”

The 91 unique ads The Markup found promote six separate credit and home equity products. We counted any unique Facebook ad identification number as its own ad, but often these are versions of the same ad that ran at different times, in different regions, or with different targeting choices.

The ads in question, which ranged from credit card ads to equity loans, appeared in data gathered by The Markup’s Citizen Browser project.

Panelists in the project automatically share data from their Facebook accounts with The Markup, including ads that appear in their news feed, plus associated information about why specific ads reached them through the “Why am I seeing this ad?” feature. In the time span of this investigation, March 16 to April 26, 2021, the panel included just over 1,800 people across the country.

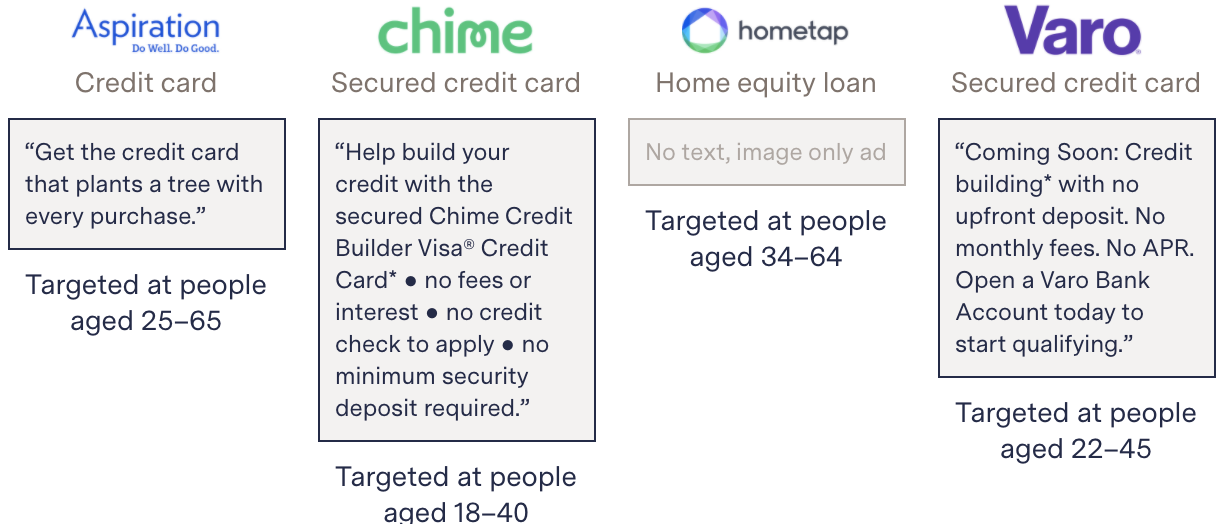

The Markup found ads from four companies falling afoul of Facebook’s own anti-discrimination policies

Targeted ad copy shown to Citizen Browser panelists

-

Credit card

An ad read “Get the credit card that plants a tree with every purchase.”

Targeted at people aged 25–65

-

Secured credit card

An ad read “Help build your credit with the secured Chime Credit Builder Visa® Credit Card* ● no fees or interest ● no credit check to apply ● no minimum security deposit required.”

Targeted at people aged 18–40

-

Home equity loan

No text, image only ad

Targeted at people aged 34–64

-

Secured credit card

An ad read “Coming Soon: Credit building* with no upfront deposit. No monthly fees. No APR. Open a Varo Bank Account today to start qualifying.”

Targeted at people aged 22–45

Facebook did not respond to multiple requests for comment.

“These are serious denials of opportunities for significant economic changes in one’s life. The ability to get a mortgage to buy a house, the ability to get a job to lift yourself out of poverty, the ability to get a loan to start a small business, the ability to get a loan to go to college,” David Brody, who leads the Digital Justice Initiative at the Lawyers’ Committee for Civil Rights Under Law said. “You have these instances in which but for Facebook’s algorithms steering these opportunities away, someone may have been able to get one of these life-changing opportunities from a business that would have given it to them.”

Aspiration, Hometap, Varo Bank, and Chime excluded certain age groups from seeing their ads, despite Facebook’s policy prohibiting age targeting in ads that “promote or directly link to a credit opportunity,” which specifically covers credit cards, as well as other financial products “including but not limited to credit card offers, auto loans, personal or business loan services, mortgage loans and long-term financing.”

It’s unclear how the ads bypassed Facebook’s filters.

Chime declined to comment for this story. Aspiration did not respond to The Markup’s request for comment.

Hometap’s head of marketing, Rachel Keohan, said it was unaware of its ads being targeted by age until The Markup reached out for comment and said it would be reviewing all its ads.

“Following your outreach, we worked with our third-party digital agency to audit our ad campaigns, and determined that many of our Facebook advertisements were, in fact, still utilizing age ranges for targeting purposes,” Rachel Keohan, Hometap’s head of marketing, said in an email. “We’re in the process of updating all of our Facebook advertisements to no longer target audiences based on age.”

“Our user acquisition team at Varo is in close contact with Facebook and discusses the nature of our ads and target audience to ensure we are fully compliant with all requirements,” Alex Woie, head of strategic communications at Varo, said in an emailed statement.

Some attorneys told The Markup that in addition to Facebook policy, age-targeted ads for things like credit cards and home financing may violate the federal Equal Credit Opportunity Act (ECOA), which prohibits credit discrimination based on factors including race, religion, gender, and age, and requires that only financial information be considered in credit applications. The text of ECOA also specifies that a creditor may not advertise services in a way that would encourage or discourage applicants according to protected classes.

Tia Elbaum, a spokesperson from the Consumer Financial Protection Bureau—the agency charged with enforcing ECOA legislation—declined to comment on the legality of targeted advertising for such products.

In addition, California’s Unruh Civil Rights Act prohibits discrimination by a business based on multiple factors including gender, ethnicity, age, medical condition, sexual orientation, and marital status.

The Markup found that nine individual Citizen Browser panelists based in California had been served at least one advertisement for financial services that was age-restricted, with some seeing the same ad multiple times. One California-based panelist was shown an age-restricted credit card ad from Aspiration; four were shown ads from Chime promoting bank accounts or secured credit cards; and six California panelists were shown ads from Varo Bank promoting accounts or a secured credit card.

The Markup did not find any ads from Hometap among the ads served to our California panelists.

Peter Romer-Friedman, principal at Gupta Wessler PLLC, who has brought lawsuits in the past against Facebook for ad targeting of financial products, including the November 2019 suit mentioned above, said the ads found by The Markup may violate Unruh if they appeared in the feeds of any Californians.

A lawsuit from last July filed in the U.S. District Court for the District of Maryland, accused property managers of targeting housing ads by age on Facebook. The defendants called the case “fundamentally flawed” in court documents, claiming that the plaintiff was unable to prove any harm from the targeted ads. (Facebook is not a defendant in the Maryland suit.)

Another lawsuit, filed in California Superior Court, San Mateo County, alleged that Facebook was allowing discriminatory practices in insurance ads. Facebook said in court documents that advertisers, not the platform, would be liable in the case. Those two cases are ongoing.

Facebook Has Long Struggled to Enforce Its Own Anti-Discrimination Policy

About a week after the settlement in March 2019 that brought about Facebook’s current ad-targeting anti-discrimination policy, the Department of Housing and Urban Development sued Facebook, alleging that the company violated the Fair Housing Act over targeted ads based on race and gender. That case is still ongoing.

About six months later, researchers found that even without intentional gender targeting, Facebook’s algorithms will calibrate themselves to show job ads mostly to the genders typically represented in a given field of work (for example, showing ads for trucking jobs mainly to men).

Last August, The Markup also found examples of advertisements for jobs targeted by age and ethnic affinity.

Sherwin of the ACLU said part of the problem is that Facebook puts too much of the onus on advertisers to comply with its policies.

“The issue is that it’s up to the advertiser to self-select that this ad is an ad for housing, employment or credit,” Sherwin said.

But Brody of the Lawyers’ Committee for Civil Rights Under Law says the platform should take responsibility.

“Facebook has built the business model around behavioral advertising and around AI algorithmic systems that are designed to profile users in a way that is very difficult, if not impossible, to disaggregate from discriminatory behavior,” Brody said.